Oil And Energy Macro Thoughts

Writings on the confusing behavior of the macroeconomics of oil.

I decided to switch my musings from a simple WordPress blog over to SubStack. I enjoy the platform and find it much easier to actually get myself to write. I have many ideas, and while things have been keeping me busy, hopefully I have found myself with a little bit of time. I have also evolved since my early writings on stocks, and I think some of the ideas I have once presented were amateur in nature. To be clear, I’m not a professional in any regard, and this is for my own enjoyment.

If you want to see some of my past write-ups or thoughts, I would check out my old Arctic Capital Blog. I am also a part of the Burry Edge discord and subreddit, so a lot of my thoughts are also there as well. In regards to my old writing, the only ones I felt proud of presenting were Ovintiv ($OVV) write-up, and my Uniqure ($QURE) investment thesis. Even than, I hope to provide a more concise direction for any thesis I present. I notice in writings I have a tendency to ramble, so I will try to stay focused for these writings.

Now that we are done with the intro, I think it’s time to present some of the ideas that have been wandering around my head and what I’ve learned.

I’ve been bullish on oil all year and continue to do so. However, I, and many other people have been wrong. I thought that Q4 2022 and Q1 of 2023 were going to be great for oil. So far, it’s been a major disappointment for anyone long oil. I wasn’t long oil itself necessarily but leveraged long certain energy stocks have not been fun. That is the first thing I’ve learned. Leverage has a place, but if you are wrong, you can easily lose money. That said, I’m beating the market this year, but down a decent amount from all-time highs.

Another lesson I’ve learned was to respect the insights of those that you don’t initially agree with. There were a couple of those who were bearish oil over the next couple of quarters that I disagreed with, but it was clear for 2022 that they were right, and I should take this into consideration and learn from it, to enhance my own framework. In reality, there was real money in being short oil after the initial spike and climb due to the Ukraine-Russian war.

Looking at the chart for crude oil, it’s clear that those who were willing to short the initial Russian war climb in crude oil generated great returns. That said, energy stocks outperformed crude oil by a large margin, providing a clear example of why it’s important to choose your instrument when you see a macro idea. I just wanted to point toward those who got it right and with explanation. Alex is an amazing insight into commodities and deserves a follow. Michael Kao also deserves a follow. Finally, I also like to point out that Marko Papic was also right. There were many others, but those were just the ones I wanted to shout out at the moment.

Why were the bulls wrong? I think there were 3 main factors that really went into oil actually returning negative returns for the year.

China lockdowns persisted for quite a long time, which lowered demand significantly in one of the largest economies in the world. There are some finer details that we have to get though on how this will play out, even with the reopening of China.

The Russia-Ukraine war had quite an impact on oil for the first half of the year, however this was short lived, and frankly there could’ve been a lot of impact from speculation at the beginning. There was this profound belief that there would be a drop in exports of Russian oil, which never did come.

Demand destruction was much higher than expected, and it’s still unclear what exactly happened and how good the data is. EIA data tends to be revised a lot, especially in 2022. There are such large disparities between weekly and monthly, that it’s been difficult to discern the United States’ demand, let alone the rest of the world’s.

Let’s talk about supply side, and what has happened thus far. Russia continued to sell their oil to anyone willing to buy, which primarily has been China and India, due to large refining crack spreads widened by high prices for petroleum products. This shifted global demand as well, as ultimately those large customers for oil started buying discounted oil from Russia. There were estimates that a large amount of Russian oil could disappear, but in reality, there was no incentive for Russia to remove their oil, and they were willing to sell at a discount. There is a ton to go at depth here, especially with the recent embargos causing Russia to scramble to find buyers for their crude. This confuses the picture, because while countries like China are more than welcoming Russia crude imports, there is only so much Russia can actually ship even with their shadow fleet of product tankers. India and China are more than happy to buy… to an extent. India doesn’t have a lot of storage avaliable, and China’s product tanks are almost topping out. This whole relationship needs to be explained in more detail.

There is not a lot of supply growth, and we did see some compare to 2021, it was a lot lower than a lot of estimates, for both OPEC and the US. This wasn’t necessarily a surprise to oil bulls, and Shubham Garg has kept on top of the fact that further growth in shale will be harder than ever, as inflation in the sector is wide spread, that those fields are simply not as profitable as they once were. Also given the recent fall in oil prices, I wouldn’t be surprised if we get further cut backs in spending on oil production growth with a lot of companies. Over the long term, this is bullish oil.

Also, OPEC+ cut production not too long ago. It looks like the right call, but ultimately the positive impact to oil prices were perhaps a bit understated to those who actually noticed what was going on. The key difference was when OPEC+ said they cut production by 2 million barrels… they didn’t cut production by 2 million barrels, they cut quota by 2 million. This is a big difference, since OPEC+ was already missing their quota, lowering the quota meant for a lot of countries, they maintained the same production. There was only a handful of countries that did cut real crude production, including Saudi Arabia and UAE. These meant that the actual might have been closer to 1.1 million barrels,1 which is a decent amount, but it clearly didn’t have the effect on oil prices as expected. Iran has actually had a lot of growth compared to pre-COVID 2020, which has been a surprise.2

Overall, capex is dry, production is more expensive than ever to grow,3 and overall this oil market volatility isn’t helping the supply issue. As we approach December, with oil prices the way they are, it won’t be surprising if we see E&P companies begin to cut back on planned growth. They will restrict CAPEX even further, focusing on shareholder returns, maintaining inventory, and paying down debt. I also want to add that most people didn't realize the SPR became a constant supply for 2022, but that should be ending for 2022, and may change to increased demand as the administration buys back oil. This is a bullish set up for the long term, and will reach a point, as the global economy consumes more energy, where demand outweighs supply by a large margin. We aren't there yet though.

Demand is the more complicated picture. We don’t have precise measuring tools and even with the tools we have, they are revised constantly with different data for different time frames. The we get a couple of tools, mainly OPEC+ estimations and EIA estimations, along with stock draws for different countries that actually have storage. I also don’t have access to other tools, like physical shipments, OilX, and Vortexa, which provide unique data.

However, we can infer what is going on based on macroeconomic trends, and we can look at the data. Simply put however, despite production picture looking not great, demand is worse. What happened to the strong demand and COVID rebound from the beginning of this year?

It was a function of a strengthening dollar, china lockdowns, and high crack spreads in my opinion. The dollar increased rapidly, effecting the demand globally by weakening most currencies, especially in Europe and Asia. This made it more expensive for these countries to import respective petroleum products. While it’s unclear how much this effected demand, it’s a factor in the big macro picture, even just comparing the price to the dollar index. While the correlation isn’t terribly strong, there is still one, as many times we see oil fall or climb depending on the dollar. Luckily the dollar has been weakening, but oil has still fallen, so it’s clearly not everything.

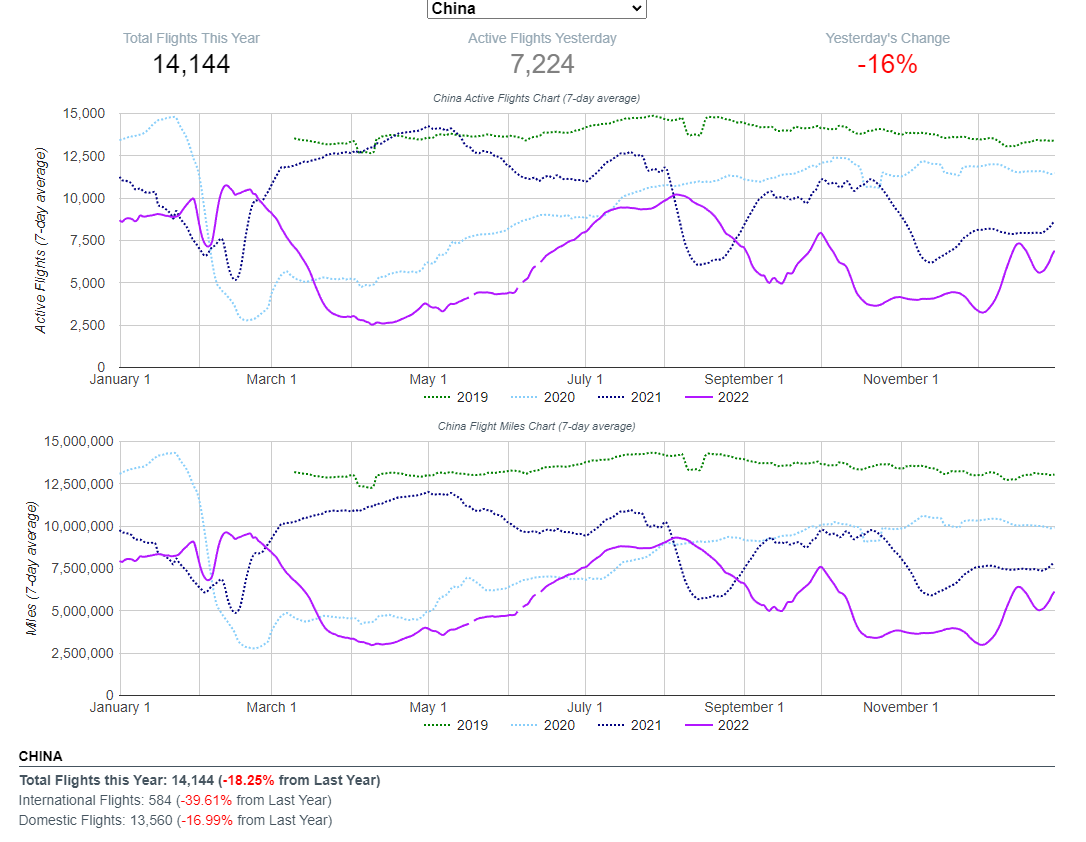

China began shutdowns again throughout the year, which didn’t help. Probably the bigger impacts are not only the falling of transportation, but the fall in demand for certain petrochemical products. Asphalt, just as an example, is a large part in the demand for crude oil in China, but that has dropped dramatically.4 There is a lot of questions about whether transportation, now that China seemingly is reopening for good, will outweigh the downfall of the real estate industry, which isn't getting any better. We should see a strong jump in jet fuel and gasoline, but China has a large amount of crude storage avaliable, and they may choose to push down crude oil by releasing it, or having their refineries use it instead of importing it.5 This essentially acts like a buffer, because if crude oil goes up very high, they could begin releasing products and crude oil from their reserves, putting a limit on oil prices. They also may start exporting more products, which we are already starting to see.6

As we move on from China, we should look at the OECD countries, because they have been the one’s lacking in demand. They haven’t rebounded to before COVID levels. There is multiple explanations for this, including more adoption of greener energy generation and consumption. I think the biggest though is a mix of life style changes and demand destruction that came from high energy prices. Earlier this year, when oil supply was still struggling keep up with demand, the spread between refined petroleum products and raw crude oil were extremely large. We saw the 3-2-1 crack spreads peak at over $60!7 This was due to low refinery capacity that was still trying to build up from the lockdowns. The increase in demand in the first half 2022 was quite strong to what was avaliable, causing prices of diesel and gasoline to jump, which wasn't helped by the chaos of the Russian-Ukraine war. This in turn lead to demand destruction, as those high prices were unsustainable. The average consumer didn't want to pay for such large prices and adjust their spending patterns accordingly. Same thing for businesses. This caused demand to sink while supply continued climbing. An example of this is the United State's consumption data, which is ugly, especially during the summer months.8

Also I like to take a quick note that gas-to-oil switching in Europe may look to be subdue compared to 3 million barrels a day predictions we saw come out swinging. Currently it’s looking like 500,000 just due to the lack of infrastructure avaliable for companies to actually make the switch.9 Perhaps this may surprise to the upside, but it remains yet to be seen. I am bullish on European natural gas, but that’s another post.

On the bright side, non-OECD countries continue to increase their oil demand, rebounding quite quickly and now are reaching new highs. We are also seeing more international flights, picking up jet fuel demand. How much can come online is debated, some suggest 2 million barrels, but if we have a lot of crude and jet fuel globally, oil prices may not benefit. Leading this charge are countries like India, which has taken advantage of cheap Russian crude oil. I do think we might’ve seen more growth if we had better global economic conditions and not as high inflation.

Based on all this, how is it looking forward? Well things change quite fast, and their is a whole slew of tail risks for oil to easily jump back to new highs. For example, war in the Middle East would surely cause jump in prices, and tensions aren’t exactly cooling over there. Also Russia cutting large amounts of production is something that should be considered, but it’s unclear how much they will actually do. There is some priced in amount of Russia crude oil that is expected to fall off due to the recent price caps, but it’s unclear how much. If it’s less than expected, say by India importing more, than it’s ultimately bearish for oil. They may choose to cut though, because Ural oil is becoming quite discounted, and shipping costs continue to climb, making it more expensive to actually ship their crude. Their margins are lower than ever on the oil they ship. I wouldn’t bet my chips on it yet, but it’s within the range of probabilities.

Things seem to change on a daily basis in crude oil, ever new piece of information we get should be analyzed. But don’t get caught up in things that look bullish, but aren’t necessarily, such as charts of US inventories falling. Also on the technical side of crude trading, liquidity seems to be low in the system, so I wouldn’t personally be surprise if we have cascade of paper selling in oil as supply outweighs demand for contracts of December or January.10 $60 WTI is on the horizon, and contango doesn’t paint a fundamentally bullish picture either. We need time to sort this all out, and volatility is still elevated in oil. So over the long-term, in this Capex cycle, things still look great, if not better. But demand is still a concern, and things haven’t improved since the beginning of 2022, and arguably have gotten worse.

To summarize supply, Russia production never truly left the market, so supply disruptions were minimal across the board.

I like to shout out to @BurggrabenH on twitter for his insights and @UrbanKaoboy as well for his thoughts. I don’t agree with them always, but they helped me understand was going on. There was also a lot more people who I stole ideas from so I could mesh them all on here for my personal framework, but they are scattered all over and it’s a lot of people to name.

We have still have to see how OPEC does with exports, but they are falling and seem to be in line with the Prince’s estimated real cuts: https://www.reuters.com/business/energy/opec-heads-deep-supply-cuts-clash-with-us-2022-10-04/. The data is still preliminary.

Despite being sanctioned, they managed to increase oil production quite significantly in 2021, and still maintaining it within 2022. I wouldn’t be surprise if we see some disruption with Iran especially the next couple of years however. https://tradingeconomics.com/iran/crude-oil-production

Oil services are experiencing shortage in supplies and in the workforce. Capital Expenditures are going up much higher than expectations for a lot of energy companies. https://www.reuters.com/business/energy/us-oil-service-firms-results-show-impact-demand-inflation-2022-10-18/.

It’s unclear how much longer the China real estate collapse has to go, but it doesn’t look like we are rebounding, which is bearish for crude demand. This article basically sums it up, and but I would make the argument it’s unclear whether the increase in transportation will off set the demand for petrochemicals. Also China might go full on SPR release since their storages are quite full. https://www.washingtonpost.com/business/energy/chinas-covid-reopening-wont-be-enough-to-save-oil-markets/2022/12/18/733a031c-7f1f-11ed-8738-ed7217de2775_story.html

China doesn’t have exact numbers for their storage, but basically if their refinery capacity is maxed out, it may be a while before we get large amounts of increased demand for oil on the open market. Again, data is hard to find, at least for me. https://www.reuters.com/business/energy/china-nov-daily-crude-throughput-rises-one-year-high-2022-12-15/

We are seeing interesting trends within the international flights picking up, potentially making more sense for China to start exporting more jet fuel, especially to other Asian countries. https://www.reuters.com/markets/commodities/china-raises-fuel-export-quotas-first-2023-tranche-consultancies-2023-01-03/

Nothing much to say, it was a great time for refineries, and still is for a lot of Chinese refineries with cheap Russian oil. https://oilprice.com/Energy/Energy-General/Can-The-Global-Gasoline-And-Diesel-Crisis-Be-Solved.html

The EIA data has been revised multiple times and their are stark differences between weekly data and monthly. However, we have to work with the data we have. https://www.eia.gov/petroleum/weekly/gasoline.php

No capacity is looking like the strong. I thought it was interesting to see Bison Interests take a bold stance and suggest upwards of 8 million barrels. They are usually right, but I don’t think they hit the mark on this one. Though if that did happen, it would be ultra-bullish oil. https://www.reuters.com/business/energy/europes-industrial-gas-to-oil-switch-stifled-by-capacity-constraints-2022-12-01/

This is a personal footnote, but if you look at the open interest for these traded features, they have begin to reach lows not seen in nearly two decades, which isn’t exactly a great sign if you are looking for an instrument to bet your crude oil on. Physical is starting to split from futures trading, or at least current contract. Unfortunately, energy stocks still seem to be tied up in this game, and physical is still opaque.